Thomas Cook Group, TCG (SP=18.25p, MCAP=£159.7m)

Thomas Cook Group (TCG) closed at 18.25p this evening, having broken up through the flattish 200 day moving average. This follows an interesting Pre-Close Statement last Friday (28th September), which suggested that business had improved - with late foreign holiday bookings being a strong factor.You may remember our previous Blog Post on 19th July 2012, when we asked if Thomas Cook was turning? Well, here at DIY-Investors, we now feel that the balance of evidence is showing that this might well be the case. So, if this is the start of a long road back to recovery for TCG, let's take another look at the evidence...

Technical Analysis

The Long Term graph doesn't make a pretty picture, as you can see:

Having fallen, from 297.5p (6th May 2009) to 10.2p on 22nd November 2011 (a drop of 287.3p, 96.57%) in two and a half years, TCG has been bumping along the bottom for some weeks.

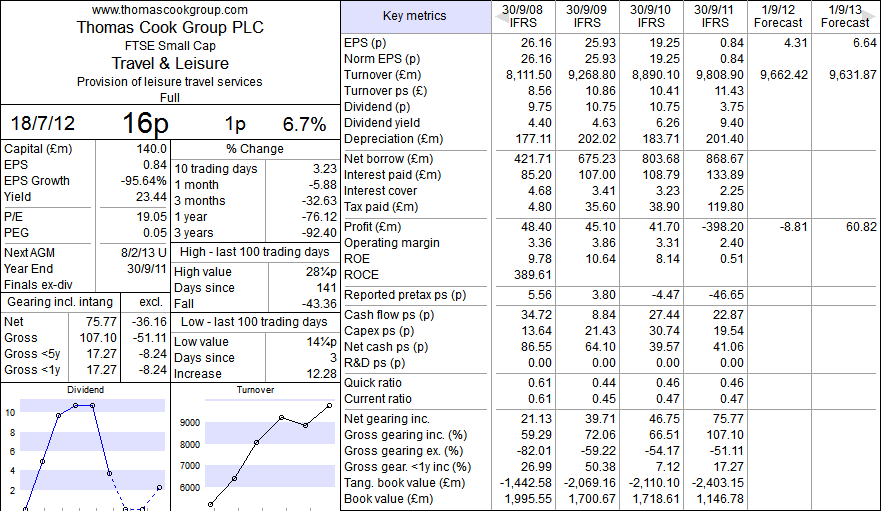

Fundamental Analysis

Trading the breakout of such a battered stock carries risk and potential reward. The Key Metrics (below), illustrate some of the problems facing TCG...

Having turned in a thumping loss last year (£398.2m), the loss is forecast to narrow considerably in the year that has just ended (on 30/09/2012).

Positive Points include:

- High Turnover but low PSR (0.16)

- Well established brand name (at least in most peoples eyes!)

- Cash-flow per share still positive last year, compared to eps (22.87p - v - 0.84p)

- Long-Term Funding in place - see Interim Results (May 2012)

- Positive action being taken to reduce borrowing (such as selling TCG India).

- High (and increasing borrowings)

- Net gearing has been rising for past 5 years

- The squeeze on household expenditures may adversely affect discretionary spending (such as holidays)

Recent Price Action (and Analysis)

The recent share price action, since the panic dump of November 2011, is worth looking at in greater detail...

You can see above that the price has clearly responded favourably to the pre-close statement last Friday. Note in particular:

- Increased volume in past two trading days

- Higher average volume last 10 or so trading days

- Buy signal on the ADX indicators (although I would like to see the 14 day ADX value higher)

- RS (against the FTSE 350 Travel & Leisure) has turned up, from a low position

- OBV has turned up

- Improving news recently (disposals etc)

- Horizontal Trading range of past 10 weeks has been broken to the upside

Let us know what you think!