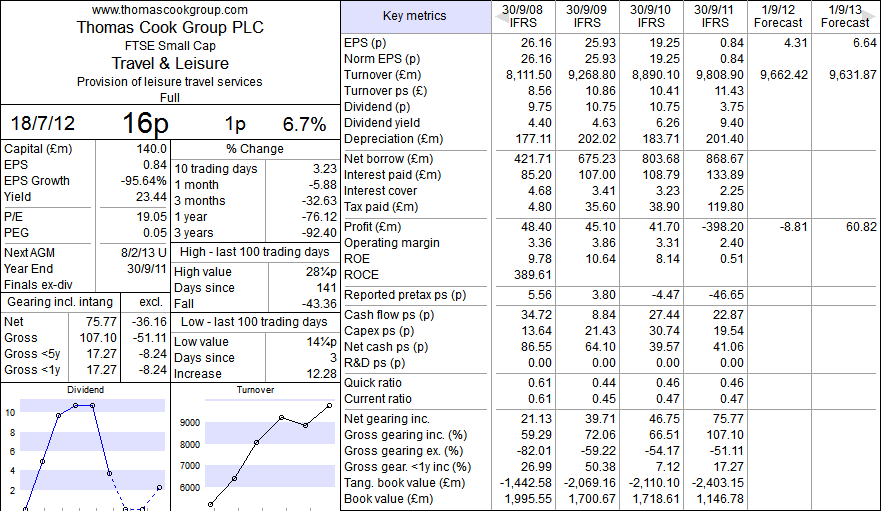

In terms of fundamentals, the Sharescope Key Metrics (below), show clearly what has been happening...

From this, you can see that the PSR(h) is only 0.014 (MCAP 140.0m / T.O. £9808m) and the PSR(pr) is 0.015 (MCAP £140.0m / T.O.(pr) £9662m), reflecting it's recent past history.

Surviving the challenges of the recession is the game for Thomas Cook and making money from successful turnarounds is one the great ways for DIY-Investors to beat the markets. So what are the factors that we should take into account in making our decision about whether to invest or not?

Well, from my research this morning, here is the position as I see it:

Technical Analysis

Having suffered a drop from 272p (Spring 2010) to the recent low of 10.2p (22nd November 2011), with a fall of 96.3% in the past 28 months or so (see below), the shares in TCG can truly be said to be "out of favour" with the smart city money.

However, there is a clear breakout from the downtrend, coupled with the following signals which you could argue are the first indications of a change of sentiment (and possible opportunity for us DIY-Investors). The short term graph (below) is very interesting!

From the initial breakout (above the 50 day m.av.), the price drifted back, went sideways but then met resistance from the downtrend line until Tuesday 17th July, when it broke through. It did this very "quietly" with no great volume to announce this to the World. Yesterday, it followed with another tick up, with slightly increased volume (but still nothing to shout about).

However, what sealed it for me was the very slight twitch (up) on the OBV, coupled with the buy signal on the ADX indicators (lower two secondary indicators above). The RSI also started to turn up.

The Debt Problem

TCG have made it clear that lowering debt has been made a priority and the Shareholders Approval (29th May 2012) to "Life Saving Asset Sales", coupled with the appointment of Harriet Green (previously boss at Premier Farnell) as the new CEO to mastermind the recovery (or should it be resuscitation?).

The proposed sale of its Spanish Hotel Chain and a 77% stake in Thomas Cook India, together with proposed sale & leaseback of some aircraft might just be enough to allow the patient to breath.

Summary

There is clearly a lot of risk in investing in TCG but having just re-read Peter Lynch's book "One Up on Wall Street" during my recent (wet) holiday in Cornwall, I can see potential reward too!

As ever, please "Do Your Own Research" and make up your own mind on this!

Mick.

No comments:

Post a Comment

Any comments on this blog? If so, please let me know!