UK Coal (LSE: UKC), closed up 5.5p (+36.8%) today at 20p - giving it an MCAP of £59.7m. This followed the final results released last Friday, which showed a return to profit for the first time in 4 years. So what's going on?

Well, first of all, let's take a look at the long-term shareprice graph...

What is immediately apparent is that UKC is in the doldrums. from the heady days of 625p a share in Spring 1996, it has yo-yo'd over the years, ending down by 98% at its recent (20 year) low of 12.18p (where it opened on 23rd April 2012). Clearly a job for St.George and the Dragon!

Looking at the past 18 months, there weren't many technical analysis clues that a possible turnaround was on the cards (see below)...

The "panic dump" on 14th March 2012, when UKC dropped by 8.25p (-27.97%) to 21.25p was on high volume (8.29m of the 299m shares issued, changing hands that day). This came about as a result of the

RNS released that day, which raised the issues of funding and re-structuring.

However, last Friday

(27th April 2012) UKC released it's preliminary results for the year ended 31.12.2011 which, despite the RNS in March, showed the following key points:

- Total Group Revenue of £488.2 million (2010: £351.2m)

- Operating profit/(loss) before non-trading exceptional items of £65.2m (2010: £(74.3m))

- Profit/(loss) before tax of £58.0m (2010: £(124.6m))

- Total production of 7.5m tonnes (2010: 7.2m tonnes), in line with expectations

- Average sales price per Gigajoule (£/GJ): £2.48 (2010: £1.97)

- Property sales of £67m achieved slightly ahead of book value

- Group net bank debt reduced to £55m (2010: £141m)

- Total net debt, including generator loan/prepayments reduced from £242m to £139m

This news was met with somewhat stunned disbelief by the market last Friday (UKC closed up 1.375p (+10.38%) for the day). However, presumably having chewed over the figures over the weekend, the market got going today, as can be seen below...

Closing up 5.5p, a gain of 36.8% for the day, UKC has certainly livened up an otherwise cool Monday. The ADX indicators (fast & slow) have registered buy signals and the OBV has also turned up nicely.

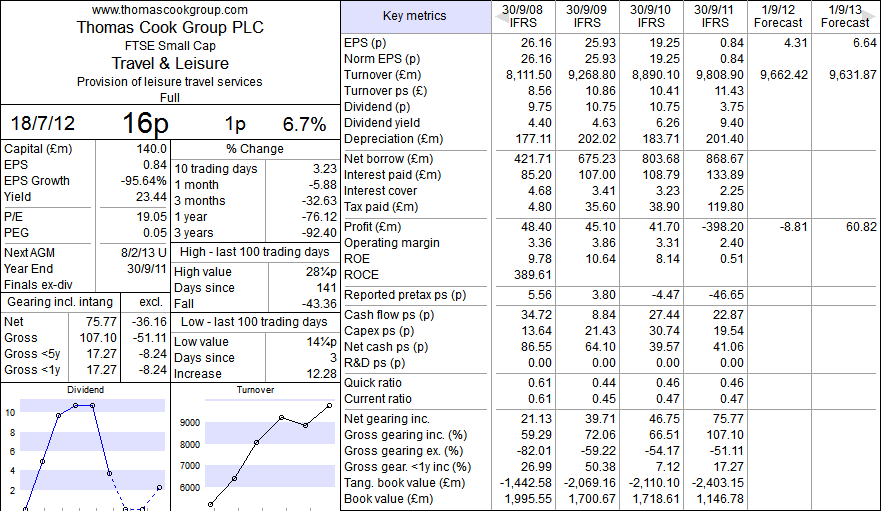

So what do the Key Metrics look like after the results? See below...

A few points to note here:

1. At the close last Friday, UKC traded with a PE below 1!

2. Even now, its PSR is only 0.12

3. Its turnover last year was up £137.02m (to £488.22m) - a gain of 39% (even with the shortfall at the Daw Mill Colliery)

4. UKC is trading below its tangible book value (even allowing for all the adverse factors affecting it - pension fund etc).

5. Its net borrowing is significantly down.

6. Its free of most of the low priced contracts and so price per tonne should increase further in the coming year.

Based on the above, you may not be surprised to hear that I've added UKC to both of my actively managed DIY-Portfolios. For those of us that have taken the plunge with UKC, 2012 could be an interesting year!

As usual, the normal caveats apply - DYOR etc.

Mick.

.jpg)